A Star Tribune letter writer today wondered how it is a young man suspected of running off to join the ISIS terror group was able to withdraw $5,000 on a debit card for financial aid at his college.

In the April 20 article about a Minneapolis mom who “has lost two sons to terror fight in eight years,” we read that her son “had withdrawn $5,000 in cash from his federal education aid debit card,” allegedly to finance an attempted overseas trip to join the terrorists.

Does our government even come close to understanding how many things are just plain wrong about this situation? Are these cards available for all American students, or do they exist at taxpayer expense for a select few while those same taxpayers struggle to finance educations for their own children?

Is this the only less-than-transparent program in existence, or are there others our government just doesn’t mention? Does the U.S. government realize that it supports terrorism through this well-meaning but incredibly naive offering?

Does our government quietly approve this jaw-dropping type of program, or do officials take the time to rationalize it to the public? I will draw my own conclusions.

Or you can do the research to get some of the answers and dispel the obvious innuendo that some immigrants are getting something the locals don’t.

Yes, the government knows about the program and released a report about it last year from the U.S. Government Accountability Office (pdf).

And there are problems with the program, the GAO said, although supporting terrorism wasn’t mentioned as one of them.

Eleven percent of the nation’s colleges and universities — covering about 40 percent of the nation’s college students — offer the option to receive financial aid on a debit card.

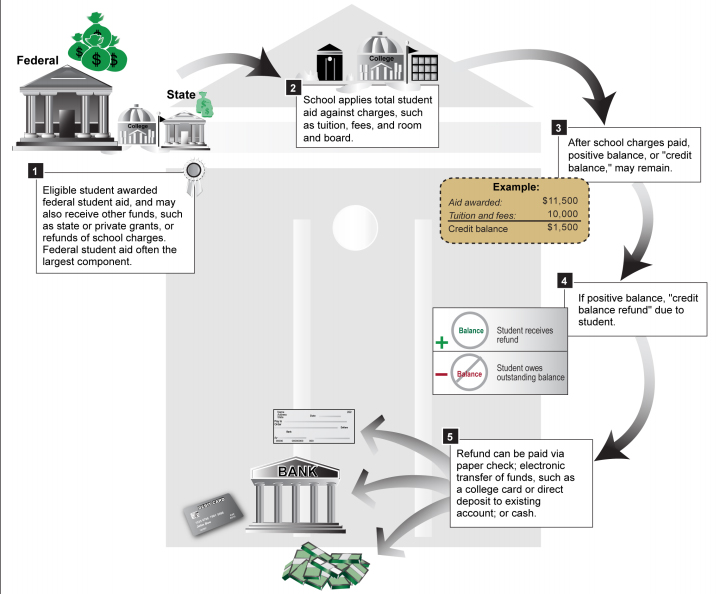

Federal student aid can be used to pay for tuition and fees, room and board, books, supplies, and other living expenses. The aid is generally paid directly to the school, which deducts its charges, such as tuition and fees.

If a student’s total payments from all sources, including financial aid, exceed the school’s charges, the school pays the difference (also known as a credit balance or credit balance refund) to the student.

The bulk of the funds paid to students may be federal student aid remaining after paying for tuition and fees, and the money is intended to help students pay for nonschool items related to their education, such as living expenses and transportation costs.

Schools can manage these payments themselves or contract with a third party to administer the process.

Schools that provide the aid via a prepaid card are generally larger institutions, the GAO said. Most of them are public institutions.

The advantages include quicker access to funds, a reduction in cash on campus, and the financial education that’s offered with the cards.

The GAO report said the problem with them is that some of the big banks that administer them take a cut of the financial aid in the form of fees.

In a 2012 Star Tribune article on the fees, Steve Sabin, president of the Minnesota State College Student Association, said the advantage of the cards is that some students “might not qualify for a traditional bank account and would have to pay hefty fees to get a cash checked.”